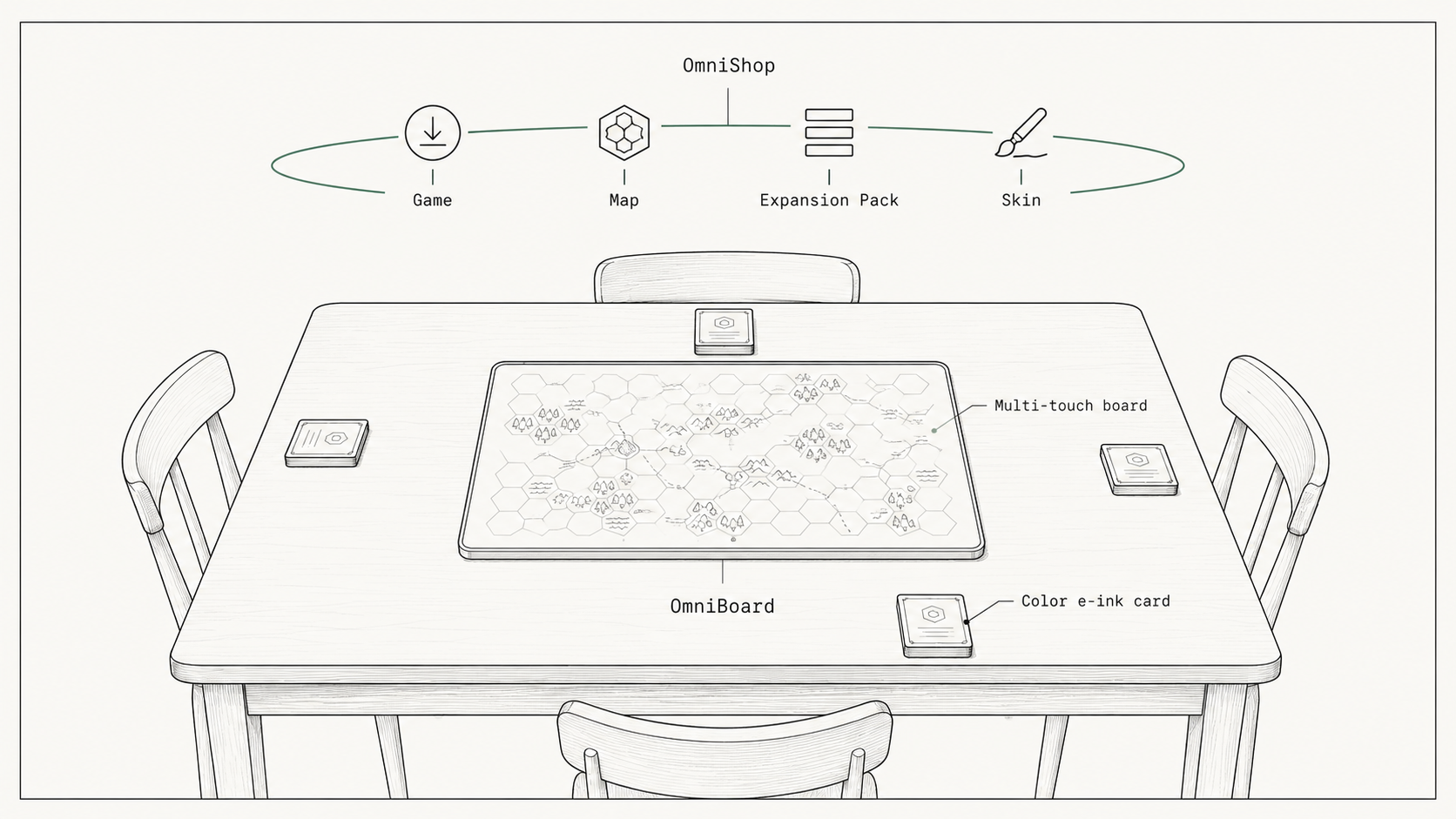

Not an app. Not a tablet. Not a companion thing that lives next to a board game. A real device. The kind of thing that sits on the dining room table, and the table feels different because it is there.

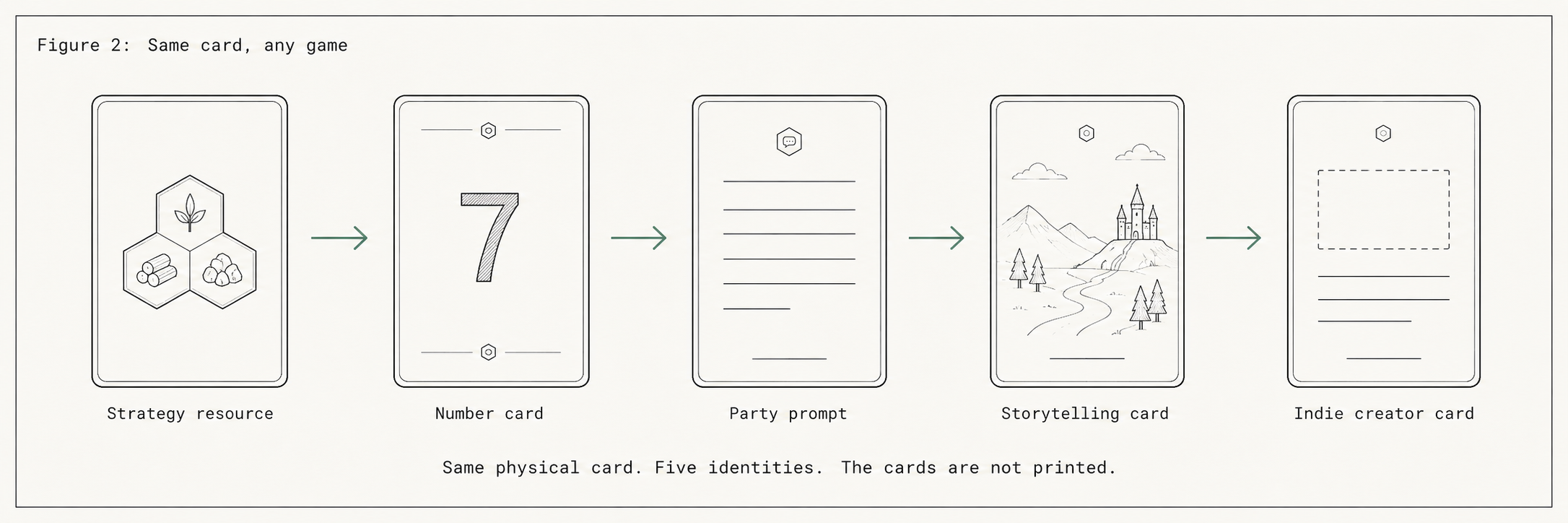

A board in the middle. Physical cards in your hand. The cards are real - paper-like, lightweight, the same shape and weight as the cards in the box you grew up with. But every card can become any card. Catan tonight. UNO tomorrow. Cards Against Humanity after dinner with friends. A new indie game next week, downloaded in thirty seconds. Same hardware. Infinite games.

That was OmniBoard.

OmniBoard started as a side project in 2023, after SNDBOX was acquired and I finally had room to write in a notebook again. It was not a company on day one. It was one of those side projects that quietly turns serious - the kind that earns a P&L, a deck, three time zones of e-ink supplier calls, VC meetings, mechanics sketched on the back of envelopes, and a marketplace design. I worked on it, off and on, through most of 2023 and into 2024.

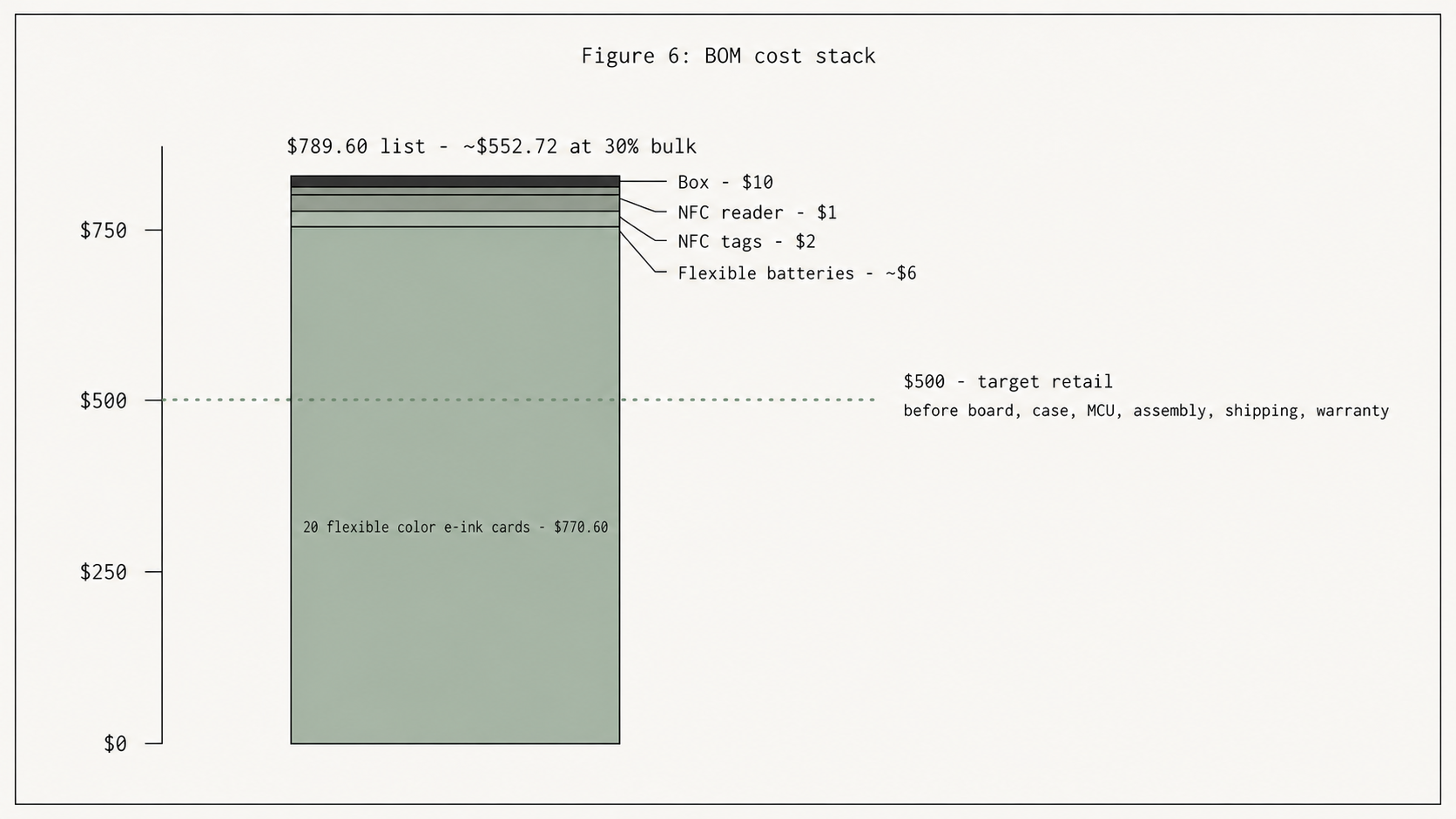

I shelved it because of one number, and that number is a real number, not a rhetorical one. I will get to it. But I do not want to start the post there. The math is the second half of the story. The first half is that this was a beautiful product and it deserved to exist.